Breakdown of the United Airlines MileagePlus Program Changes.

Recently, United Airlines MileagePlus announced that from November 15th, 2019, the program would be changing.

The program will be moving away from fixed Saver and Everyday fixed miles rates, and removing the award chart.

That means MileagePlus members will lose transparency on the number of miles required to book a flight – until the member does a real-time search.

What are United Airlines management thinking and what is the thought logic behind the changes?

What are the financial and non-financial outcomes for United Airlines?

Are there non-financial risks that United Airlines had to factor into the decision-making process?

Let’s get into it.

If you’re not familiar with the United Airlines MileagePlus program, check it out.

This analysis is broken down into three key areas.

-

Benefit vs Cost Comparison

-

Non-core FFP Benefit vs Risk

-

Member and Market Sentiment

1. Benefit vs Cost Comparison

a) Direct Revenue Benefit vs Direct Revenue Cost

Direct Revenue Benefits:

- Greater fare recovery on award inventory when sold to members at higher miles cost.

Direct Revenue Costs:

- Removal of $75 close-in booking fee

- Award inventory that would previously be sold at higher miles cost now being priced at lower miles cost, and thus, reduced fare recovery [direct negative impact on RASM]

b) Indirect Revenue Benefits vs Indirect Revenue Loss

Indirect Revenue Benefit:

- Should more miles be burned overall, revenue recognition (ASU Topic 606 / IFRS 15) will increase.

- Increased RASM if more inventory is sold at higher miles rate than the current rates.

- A cashflow increase from extra miles created into existence.

Indirect Revenue Loss:

- Reduced breakage will put additional pressure on margins

- Buy, Share and Gift miles sales will take a hit. As the value of miles decreases, it will become more difficult to sell bulk loads of miles directly to members

at a premium. - Cost per mile to other non-air third parties. It’s difficult to look at a partner in the face and say $0.035 per mile is the going rate when the burn rate on United Airlines flights is taking a 50% devaluation on the back end. Smart third parties will be looking to some form of goodwill from United Airlines (price reduction, bonus marketing etc..)

- Decreased RASM (if more inventory is sold at lower miles rate than the current prices).

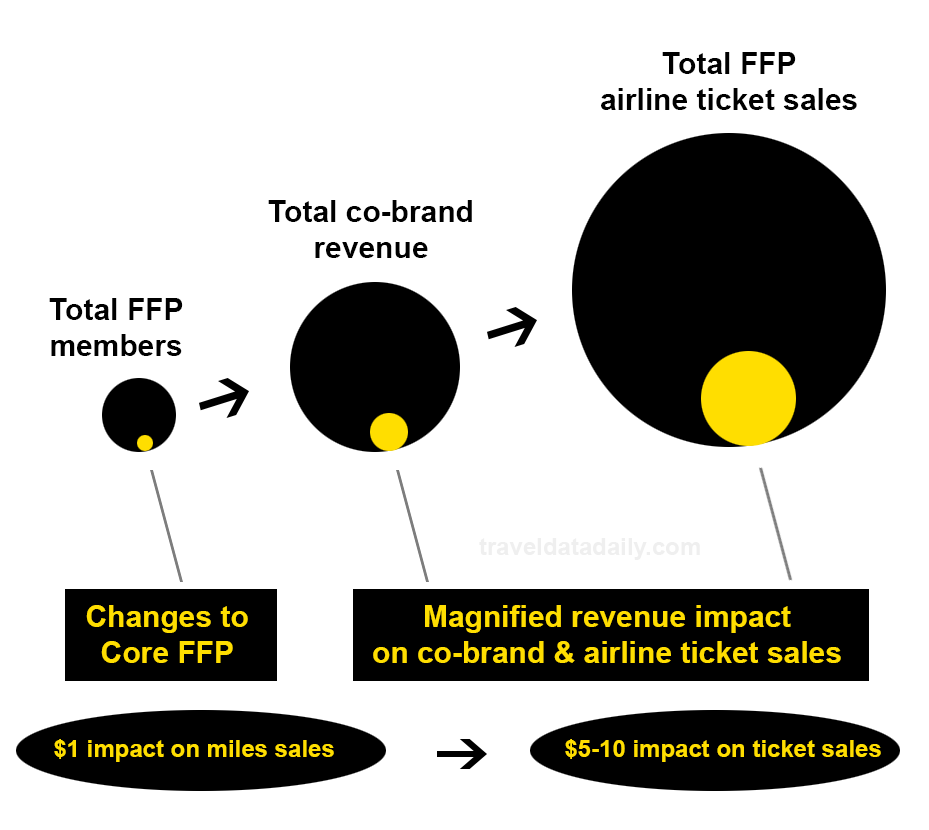

- Airline ticket sales impact

Loyal frequent flyers tend to spend more than non-loyalty members, so any revenue loss from core FFP base will require additional marketing investment so the revenue gap is made-up by non-loyalty program members.

c) Non-financial Benefits vs Non-financial Loss:

Non-financial Benefits:

- Potential increased inventory for members, thus improved program attractiveness.

- Greater pricing control of award inventory for the airline and less friction internally between departments.

- Greater insight into the pricing sensitivity of member segments (behavioural data could be applied to drive up cash fares)

Non-financial Loss:

- New membership signups to MileagePlus from non-US members will decrease as the program loses attractiveness versus local alternatives (in other markets) for these travellers.

- Decreased program value by US members when compared to other players in the market, depending on the segment of traveller.

2. Non-core FFP Benefits and Risks

Co-Brand Specific Risks

- United has struggled to meet co-brand targets over the past two years. This lead to the changes in the United Explorer card. Can United Airlines and Chase afford further perceived negative impacts to the program?

- Frequent spenders (members earning miles from card spend) are not necessarily tied to any airline since they’re not frequent flyers. As the aspirational value of United Airlines awards decreases compared to the competing frequent flyer programs, the attractiveness of the program to this segment of frequent spenders will decrease.

The risk of negative impact to United’s cobrand revenue growth is real – there is a sizeable risk that customers will no longer desire to collect the airline’s currency and will instead focus on other reward options such as cash-back cards or bank rewards programs.

This doesn’t mean that United will see a reduction in cobrand revenue – far from it. But the opportunity cost of a reduction in growth can be material.

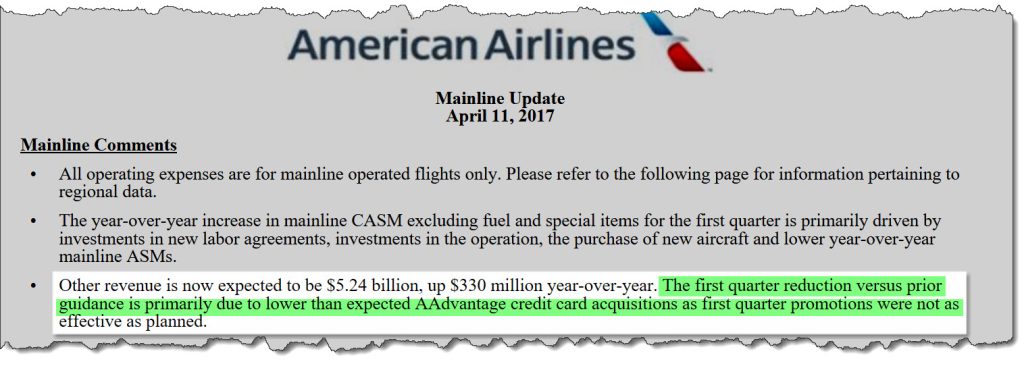

In fact – American suffered this same fate as a result of its 2016 program devaluations, despite signing its much-heralded new co-brand agreements with Citi and Barclays (the higher-price-per-mile model which Scott Kirby now wants to realize from Chase at United).

American’s April 2017 SEC 8-K filing reveals that American had to lower its revenue guidance by $20 million, due to customers turning their backs on the AAdvantage mileage currency.

The new credit card deal with Citi & Barclays was forecast to generate an additional $350m year-over-year. This forecast has been downgraded to $330m.

This expected $20 million loss virtually wipes out the $24.3 million in estimated savings from recent program changes.

In the psychology of loyalty programs article, David talks about the importance of having a clear [redemption] goal in mind, so that loyalty members are able to strive towards their target.

In the absence of a target (eg: moving goalposts), the psychological effect that has on consumers is that of disengagement.

Other potential benefits:

- Greater inventory to members will be perceived as a positive move. Shifting a redemption away from non-air redemptions (eg: hotels, apple, etc) may help keep cash within the group.

Other potential risks:

- Chase will undoubtedly see an immediate influx of mileage transfers into United.

The first wave will start now, as savvy members burn their miles for travel prior to Nov 15. The second (permanent) wave will be after Nov 15. As more miles will likely be required for travel, this will increase the miles being created into the MileagePlus program. As such, Chase is footing the bill for the program changes.

If Chase were smart- they would be negotiating a lower rate per mile for the increase in miles volume.

The associated other risks have the potential to hurt the marketing revenue as the margin on miles will decrease.

- Should American Airlines give up their competitive Advantage and blindly copy Delta Airlines and United Airlines, the risk to United is that a segment of members will disengage entirely from full-service carrier loyalty programs. Frequent flyer programs all over the world are shooting their own feet by devaluing their programs, and these changes drive up the value of low-cost airlines.

3. Member & Market Sentiment

A pure risk vs reward analysis highlights a glaring truth. The downside risk from the program changes overshadows the potential upside.

To see how the changes play out for United Airlines will ultimately depend on three factors.

- If AA copies UA/DL and becomes another me-too program.

- If Chase wises up and brings their big guns to the negotiation table to drive down the cost per mile.

- The % of members who will disengage with the program, and their associated air miles+non-air miles+ticket sales revenue United loses from that. Given the nature of the program changes, United cannot realistically expect any segment to spend-up on ticket sales.

But, Delta did it…??!

A key driver of these changes is the desire from management at United Airlines and American Airlines to copy Delta – in the hope that they will realize the revenue premium that Delta enjoys.

But Delta is a very different airline with very different fortress hub economics.

Delta also commands a revenue premium, not because of its SkyMiles program – but because it is regarded as running a superior airline operation. This, in turn, allows it to leverage additional revenue from its SkyMiles cobrand agreements.

In contrast – United Airlines and American Airlines need to rely on their FFPs to drive passenger behaviour and revenue as the underlying airline operations are inferior to Delta.

Messing with the FFP from a position of core airline weakness is seldom a smart strategy.

When airlines change their frequent flyer programs, it has a genuine behavioural impact on how passengers interact and spend with the airline.

These can be good or bad. For Cathay Pacific, changing their Marco Polo program cost $1B in enterprise value for the company.

It’s straightforward that – if the program is improved- people will become more engaged and fly more with that airline.

If the loyalty program changes to the detriment of members, then members will fly and spend less.

Where to from here?

With the above insights in mind, United will likely see short term [9-12months] revenue gains. Beyond the next 12 months will depend on the cards that American Airlines and Chase play next.

Your move, American.